According to a study in the Annals of Family Medicine, the average amount of time that a doctor...

August 26, 2019

The healthcare system in the United States is once again poised for upheaval. It has only been 11 years since Congress passed the Patient Protection and Affordable Care Act (PPACA), popularly labeled Obamacare, but new political and societal groups are eager to make healthcare a government-sponsored entitlement for everyone. A multitude of proposals that largely focus on expanding Medicare has shaken the fragile U.S. healthcare sector, and if Congress does pass one, it could tip the system into chaos.

Originally established in 1966, Medicare is a national health insurance program for Americans 65 and older. Last year, Medicare insured more than 59 million Americans using funds from payroll taxes and out-of-pocket fees from beneficiaries. Medicare currently consists of four insurance programs: inpatient services, outpatient services, prescription drugs, and managed Medicare. In 2018, Medicare’s total annual expenditure reached $582 billion.

Many supporters of Medicare For All argue that healthcare should be guaranteed in the world’s richest nation, but critics contend that such a radical change would cripple the U.S. economy and deal a death blow to health insurers and struggling healthcare providers.

There are four important questions that policymakers appear to either ignore or fail to consider when evaluating the viability of a universal healthcare system managed by the federal government:

- The smartest young minds that are considering healthcare as a career choice already have a tough decision to make, considering the extended education (and debt) required to be a doctor or nurse. How many will make that career choice when the result, after all the additional school years and debt, is that they are fundamentally a government employee? Common sense begs the question that the smartest minds will choose a different career path, leaving the US healthcare system with sub-par caregivers.

- Does it make social or economic sense to raise taxes for 100% of Americans just so the 20% that use healthcare services in any given year don’t have to pay anything out-of-pocket?

- Why are all the proposed solutions centered around free healthcare? Having a roof over our heads is as important as healthcare, yet no one is advocating to raise taxes to give away free homes to every American. Wouldn’t a better result be achieved by expanding healthcare financial literacy and letting the free market address the affordability barrier associated with out-of-pocket healthcare costs like the mortgage industry did for homeownership? Wouldn’t the sustainable solution be to make healthcare costs more affordable instead of free?

- Shame on us if we don’t learn from past mistakes. Medicare & social security are worthy and noble social programs, but when left to the government to manage, both of those programs would have collapsed if the government didn’t reach into our pockets through additional taxation to save them. Where is the evidence to support the idea that expanding Medicare for all won’t result in the same government mismanagement?

How Medicare Has Performed So Far

Prior to President Lyndon Johnson signing the Social Security Amendments of 1965 that founded Medicare, only 60% of American seniors had health insurance. The program extended coverage to almost all Social Security beneficiaries, which have grown as a population from 20 million in the 1970s to almost 60 million in the present day.

Medicare typically covers about 80% of approved medical expenses with the remaining 20% left to the patient to pay out of pocket. Medicare does not cover vision, dental or long-term care.

Most Medicare enrollees would agree that the insurance program provides an indispensable safety net for American seniors. While this may be true, many healthcare experts argue that the program has been disastrous for U.S. healthcare. An analysis of U.S. healthcare expenditure shows that costs remained relatively flat up until about 1970, at which point, costs embark on a trajectory far outpacing economic growth.

In other words, shortly after the introduction of Medicare, healthcare costs grew much more rapidly than the rest of the economy. The National Bureau of Economic Research issued a paper suggesting that this surge is directly related to the injection of capital that Medicare produced. If true, increased participation of the government could incentivize healthcare providers to inflate prices.

How Medicare For All Would Reshape the Healthcare Landscape

Among the many possible Medicare For All proposals, the most popular components include:

- Health coverage for all residents in the U.S.

- The program would be funded by a trade tax on Wall Street

- The government would reimburse healthcare providers for services rendered

- Patients would pay no out-of-pocket expenses

- The government would negotiate pricing with providers including hospitals, vendors and drug manufacturers

Universal health coverage has long been an aspiration of key American demographics, spurred on largely by other major industrialized nations with single-payer health insurance. Unfortunately, many of these foreign healthcare systems have glaring defects that American consumers would probably find unacceptable.

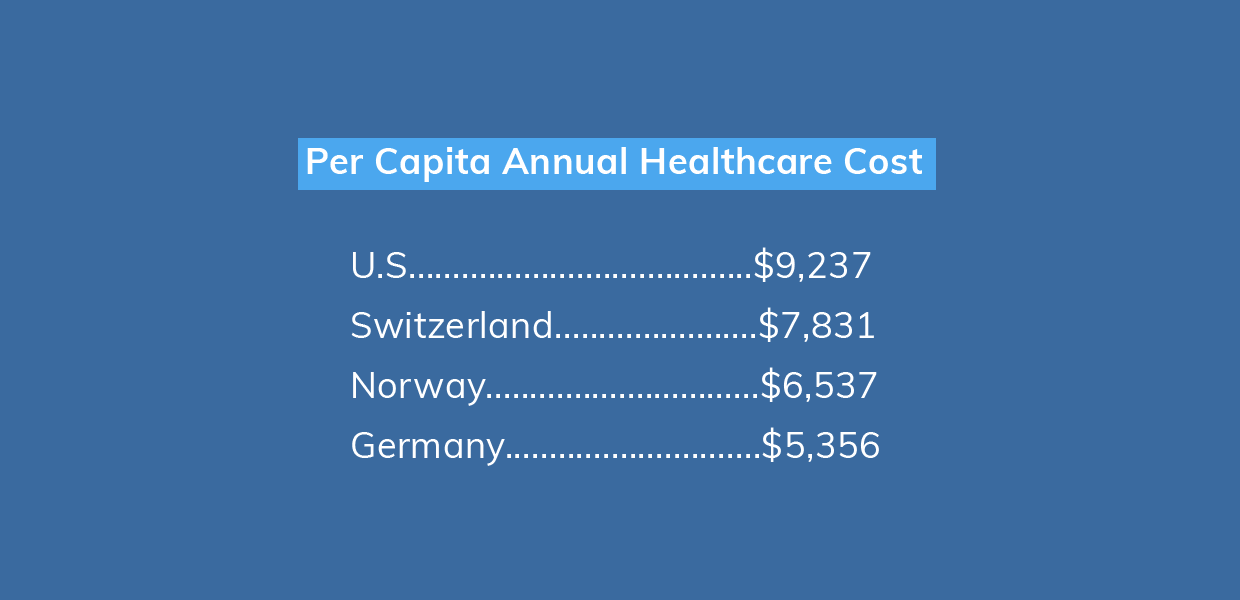

The biggest obstacle to implementing Medicare For All is, of course, the enormous cost. Many supporters contend that such a system would ultimately bring down healthcare costs for all Americans. This is based on the fact that the U.S. is the only major industrialized nation without universal coverage and that the per capita annual healthcare cost is $9,237, far ahead of our next leading competitors Switzerland ($7,831), Norway ($6,537) or Germany ($5,356).

While there is the potential for cost savings at some point in the future, there are some virtually insurmountable transition costs. For example, the Medicare For All proposal set forth by Vermont Senator Bernie Sanders would impose a new tax on Wall Street’s hedge funds, investment houses and other trade entities. Though critics feel this enormous tax hike would almost certainly stall economic growth and lead to more unemployment. The majority of the proposals for universal healthcare also incorporate raising taxes for individual Americans, including the middle class.

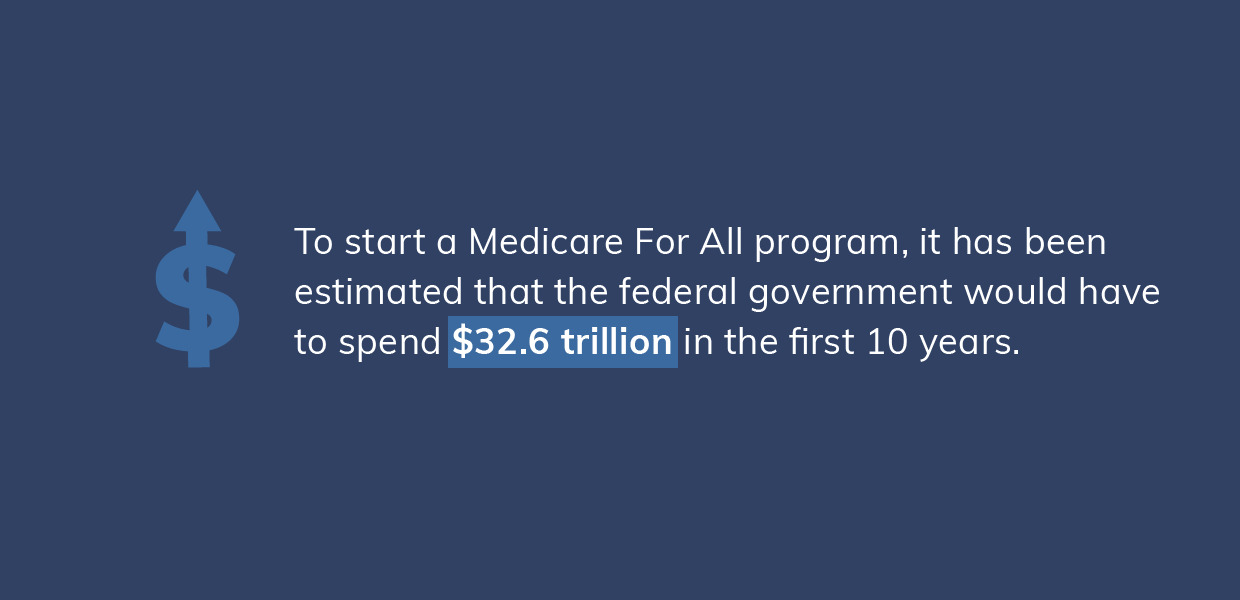

To start a Medicare For All program, it has been estimated that the federal government would have to spend $32.6 trillion in the first 10 years. This amount dwarfs all of the current revenue for the federal government, so it would likely have to borrow heavily or increase individual taxes dramatically, putting the entire economy at risk.

The financial challenges of implementing universal coverage are only some of a multitude of potential pitfalls. Almost the entire healthcare community recognizes that the U.S. industry could be severely damaged by a precipitous move to socialized medicine. Following the disastrous rollout of the PPACA in 2008, the cracks in the system became increasingly evident including a less competitive healthcare business environment and unsustainable strain on a limited physician population.

The Promise of Medicare For All

The ultimate goal of Medicare For All is to guarantee health coverage to all U.S. residents. This is a laudable goal and one that should be achievable in the world’s singular superpower. It is conceivable that a Medicare For All program could be extended incrementally over a long period until the entire U.S. population is covered. Such a possibility labeled the public option--in which Americans younger than 65 could enroll in Medicare--has been previously floated in Congress.

In addition to universal coverage, the appeal of Medicare For All lies in its supposedly diminished out-of-pocket cost to American households. The enormous expenditure on filing claims with government agencies and private insurers, as well as billing patients increases costs for American households by almost half. But the math doesn’t line up; increasing individual taxes that are paid every year is more of a burden on American Households than paying out-of-pocket costs that are only due when you actually receive care.

Whether Medicare For All becomes a reality or not, the U.S. healthcare system must remain viable. That means that coverage should be broadened to include as many as possible while keeping costs reasonable. It appears that universal health coverage will take years or decades to fully realize, so we should do our best to make existing medical services as accessible as possible. US consumers play a vital role in the healthcare ecosystem, however, it is the industry’s responsibility to break the affordability barrier and enhance the consumer's financial experience through pre-care engagement, expanding healthcare financial literacy & cost transparency, and offering affordable payment options.

FinPay is a nationally recognized leader in patient financial management. FinPay’s platform is breaking the affordability and financial literacy barriers in healthcare. A six month study revealed that patients have given FinPay a 99% satisfaction score for their financial experience with FinPay. If you would like to enhance your patient's financial experience and get paid for the services you provide please contact FinPay to schedule a consultation.